Industries /

Farming & Agriculture

Cash doesn't come in at harvest. The bills do.

Equipment breaks down in the middle of a season. Input costs get committed months before the crop pays out. A bad yield doesn't pause the loan. We work with farmers who run real operations and need capital that understands how agriculture actually works.

Farming businesses are capital-intensive by nature. Seed, fertiliser, feed, fuel, equipment — the costs run continuously whether the season is producing or not. Revenue arrives in concentrated windows that can be months apart. Traditional lenders underwrite for monthly consistency. Agriculture doesn't work that way. We work with lenders who understand seasonal cash flow, production cycles, and the difference between a farm that's struggling and a farm that's simply in a gap between input costs and income.

We work with arable and crop farmers, dairy operations, and livestock producers. Your bank statements look lumpy because your business model is seasonal, not because your operation is weak.

The situations farmers actually call us about.

These aren't edge cases. They happen on farms every season. Mach works with farmers who are dealing with exactly these problems right now.

The seed and fertiliser bill is due in March. The harvest doesn't pay until September.

You know exactly what you need to plant this season and what it will cost. Seed, fertiliser, crop protection, fuel — the inputs are committed months before a single tonne moves. If you're waiting on last year's crop payments or a delayed BPS subsidy, you're staring at a six-month gap between your biggest outgoings and your biggest income.

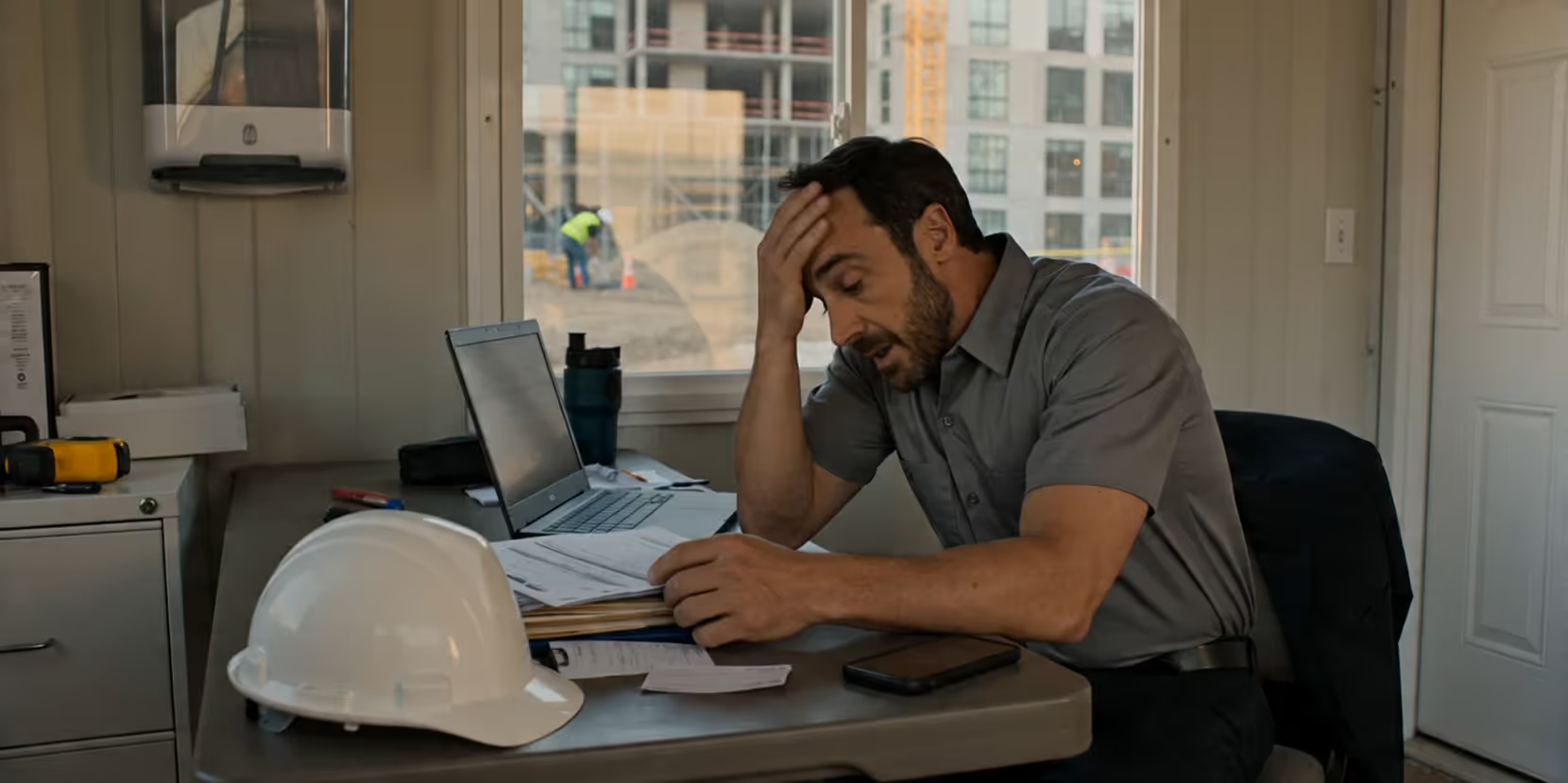

What goes wrong without capital

A combine failure in August doesn't wait for your bank to respond.

Harvest equipment going down mid-season is one of the most expensive things that can happen to an arable operation. Every day offline is yield left in the field. Repairs or contractor hire costs can run to tens of thousands — and the timeline for a traditional loan approval has nothing to do with the timeline of a crop that needs to come in before the weather turns.

What goes wrong without capital

A parlour equipment failure stops production. The milk processor doesn't pause your contract.

A milking parlour breakdown — pump failure, cooling system, automation fault — can halt an entire dairy operation within hours. The repair or replacement cost is immediate. The milk contract obligations and the daily feed bill don't stop. You need capital that moves as fast as the problem does.

What goes wrong without capital

You need to buy store cattle in autumn. The sale cheque isn't coming until spring.

Livestock farming runs on a buying-and-selling cycle that can span six to twelve months. Store cattle or finishing lambs purchased in autumn won't generate income until they're sold — often six months later. The purchase cost, the feed through winter, the vet bills, and the housing costs all run ahead of the return. A beef or sheep operation that's fundamentally profitable can be cash-flow negative for the majority of its cycle.

What goes wrong without capital

From the people we work with.

"I wasn't sure at first if this was possible or real but Noah assured me it could be done. I needed money to win a project and fast.I had to get the funds or I would lose the contract within 24 hours... Noah had me send over the documents needed to achieve the funds, Allan worked his magic, and was able to get me approved for more than what i needed! I only took what i needed now but it feels good to know that if anything changes I have access to more funds very quickly. Thank you Noah and Allan!"

"Tony Bode is excellent at his job. He is very knowledgeable and went above and beyond to offer multiple options to best fit our business needs. I would highly recommend dealing with him if business funding needs arise for your business as they did for my business. Thank you again Tony and MACH funding."

"I found out about Mach Funding about a month ago, I applied but was not approved. But the process went exactly how Kelly explained it to me. Easy process and honest people to do business with. No gimmicks a very straight forward process. Thank you to Kelly for explaining how the product works and giving me the website to apply. I will be letting my colleagues and business partners know about Mach Funding."

"I have worked with Tony from Mach. He has always gotten back to me quickly and been able to secure funds within 24 to 48 hours. I will continue to use them for my capital needs."

"I want to take the time to thanks for extraordinary customer service provided by Mac Funding team: Michael Rodriguez, Tony Bode and Azi Sharbani. Thank you for taking the time for explaining every aspect of the loan offers and obtain the best loan that fit my financial circumstance. Thank you. Thank you, and Thank you."

The questions business owners actually ask. Straight answers.

No. Seasonal revenue is one of the most well-understood patterns in agricultural lending. The lenders in our network who work with farming businesses underwrite for your annual revenue and your cycle, not your slowest month. Your advisor looks at the full picture.

Yes — that's one of the most common use cases in agriculture. Seed, fertiliser, crop protection, feed — committed before income arrives. Your advisor sizes the advance to your seasonal input exposure and structures repayment around your harvest or sale window.

Yes. A delayed subsidy payment is a predictable, temporary gap — the money is coming, the timing is the problem. Working capital bridges that gap and repays when the payment arrives. Tell your advisor what you're waiting on and they'll structure it accordingly.

Yes. Agricultural banks decline profitable farming operations regularly because the cash flow looks irregular on paper even when the business is fundamentally sound. The lenders we work with understand the farming business model. A bank decline is not a Mach decline.

Yes. Emergency working capital for equipment failure is one of the situations we handle most urgently. Many clients fund in 24 to 48 hours from a completed application. If you have a combine down or a parlour failure, tell your advisor on the qualification call — they know which lenders move fastest.

There's no minimum acreage or herd size. The requirements are at least 3 to 6 months of operating history as a business and at least £8K to £10K per month in revenue. The qualification form takes 5 minutes and your advisor tells you honestly what's available for your situation.

Find out what you qualify for. Five minutes.

No credit pull. No bank statements at this stage. Your advisor reviews your situation and tells you honestly whether Mach can help before you commit to anything.