Industries /

Restaurants and Food Service

The restaurant business doesn't give you 30 days to figure it out.

The walk-in fails Friday afternoon. The second location deposit is due in 10 days. Fall inventory gets committed in August or you pay October prices.

Restaurant cash flow is real, consistent, and completely unpredictable on any given day. Capital moments arrive without a calendar notice. Most traditional lenders look at that variability and step back. We built our lender relationships around it.

We work with full-service, quick service, catering, and food production businesses. Your daily transaction volume tells a story that a balance sheet does not.

We work with lenders who underwrite on that story.

The situations restaurant owners actually call us about.

These aren't edge cases. They happen in kitchens and dining rooms every week. Mach works with restaurant owners who are dealing with exactly these problems right now.

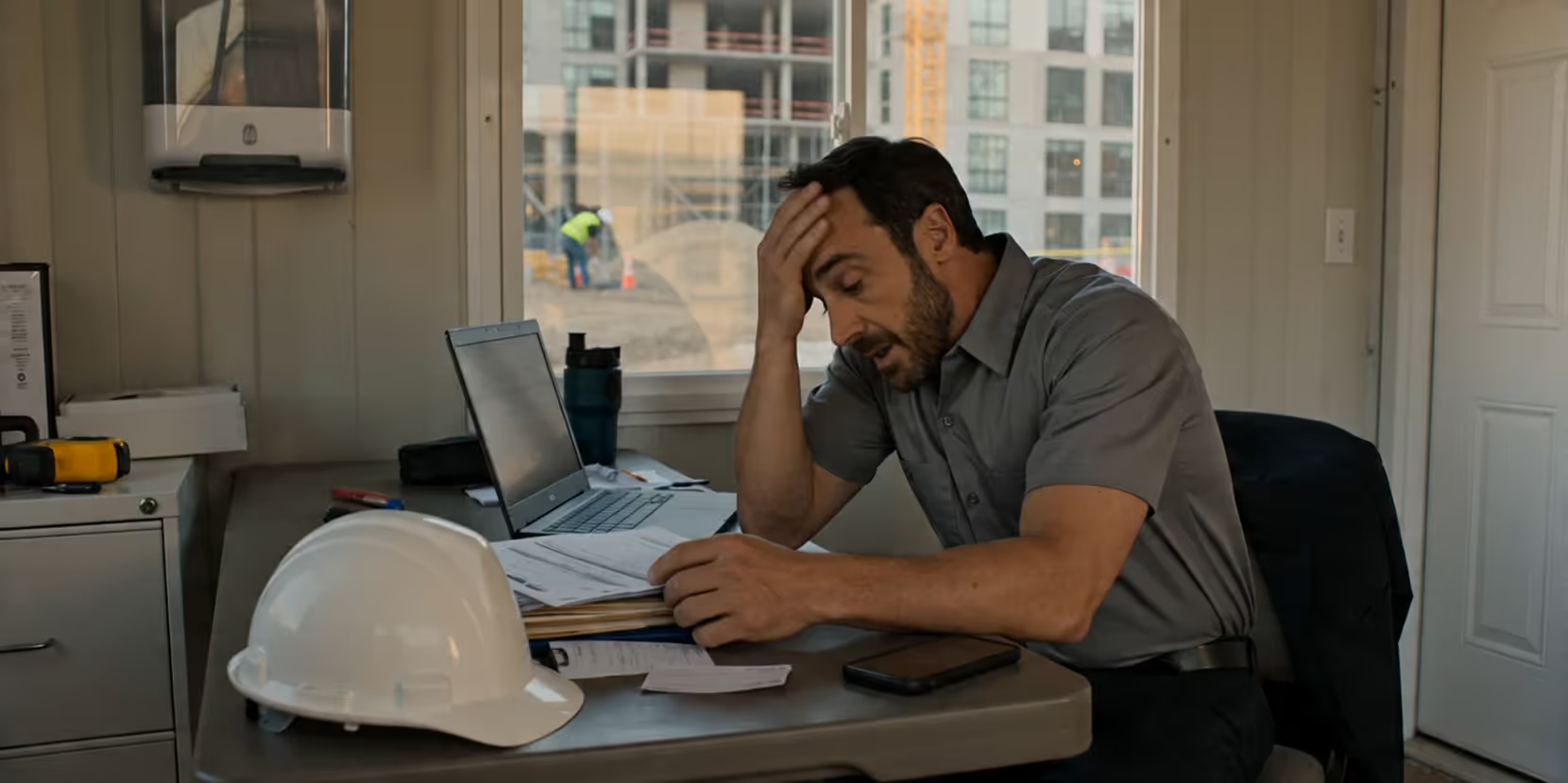

The walk-in compressor failed on a Friday. You'll need capital by Friday afternoon

A walk-in failure isn't just an inconvenience — it's a potential $15,000–$40,000 loss in spoiled inventory on top of a $5,000–$15,000 repair or replacement bill. Banks don't move over a weekend. Your food cost is already gone. You need capital today, not in two weeks.

What goes wrong without capital

You commit to fall inventory in August or you pay October prices.

Restaurant margins depend on locking in supplier pricing early. Fall menu ingredients — proteins, specialty items, dry goods — get committed in late summer. If you wait until you need them, the price is 15–25% higher and your margin is gone before the guest sits down.

What goes wrong without capital

The lease is signed. The deposit is due in 10 days. You haven't served a plate there yet.

Expanding to a second location requires a lease deposit, buildout capital, equipment purchases, and initial staffing — all before the location generates a dollar of revenue. The first location is profitable. But it can't fund the second one and run itself at the same time.

What goes wrong without capital

A private event or catering contract requires temporary staff you can't float to the next pay cycle.

A wedding catering contract or a corporate event booking comes with a significant labor requirement. The event pays after completion. Your servers, bartenders, and kitchen staff need to be paid on time regardless of when the client's check clears.

What goes wrong without capital

From the people we work with.

"I wasn't sure at first if this was possible or real but Noah assured me it could be done. I needed money to win a project and fast.I had to get the funds or I would lose the contract within 24 hours... Noah had me send over the documents needed to achieve the funds, Allan worked his magic, and was able to get me approved for more than what i needed! I only took what i needed now but it feels good to know that if anything changes I have access to more funds very quickly. Thank you Noah and Allan!"

"Tony Bode is excellent at his job. He is very knowledgeable and went above and beyond to offer multiple options to best fit our business needs. I would highly recommend dealing with him if business funding needs arise for your business as they did for my business. Thank you again Tony and MACH funding."

"I found out about Mach Funding about a month ago, I applied but was not approved. But the process went exactly how Kelly explained it to me. Easy process and honest people to do business with. No gimmicks a very straight forward process. Thank you to Kelly for explaining how the product works and giving me the website to apply. I will be letting my colleagues and business partners know about Mach Funding."

"I have worked with Tony from Mach. He has always gotten back to me quickly and been able to secure funds within 24 to 48 hours. I will continue to use them for my capital needs."

"I want to take the time to thanks for extraordinary customer service provided by Mac Funding team: Michael Rodriguez, Tony Bode and Azi Sharbani. Thank you for taking the time for explaining every aspect of the loan offers and obtain the best loan that fit my financial circumstance. Thank you. Thank you, and Thank you."

The questions business owners actually ask. Straight answers.

It's actually designed for it. Revenue-based repayment takes a percentage of your daily card volume — which means lower payments on slower days and faster payoff on strong ones. It flexes with your revenue rather than imposing a fixed installment.

For emergency situations — walk-in failure, critical equipment — we have lenders who move outside of standard business hours. Tell your advisor what the situation is on the qualification call. The answer depends on your specific lender match.

Yes. Slow-season cash gaps in the restaurant industry are predictable and well-understood by the lenders in our network. Your advisor looks at your annual revenue and structures accordingly — not just the slow months.

At minimum: 2+ years of operating history on the first location, consistent revenue, and a clear picture of the second location's timeline and cost. Whether that's working capital or an SBA loan depends on your credit profile and how much time you have. The qualification call is the fastest way to find out.

Your advisor sizes the advance and repayment structure to your actual revenue. We don't push a product that creates a new problem. The cost of capital is explained in plain language before you sign — factor rate, total payback, daily payment — so there are no surprises after the wire.

Yes. Banks decline profitable restaurants for reasons that have nothing to do with the quality of the business — inconsistent months, irregular deposits, seasonal patterns. The lenders we work with underwrite restaurant businesses for what they actually are. A bank decline is not a Mach decline.

Find out what you qualify for. Five minutes.

No credit pull. No bank statements at this stage. Your advisor reviews your situation and tells you honestly whether Mach can help before you commit to anything.